You’ve sold your home. Now the IRS wants your money.

- Practical Intelligence

- Jul 12, 2019

- 2 min read

Calculating taxes on real estate sold.

A number of people I know have been selling their homes lately and there are many questions regarding Capital Gains on home sales. First a few definitions.

Capital Gains:

Capital gains are the amount of money you’ve made above the basis of your home

Basis:

The Basis is basically what you bought the home for, plus improvements

Selling price:

What you sold your home for (less selling costs, which we won’t get into).

Exclusions:

The government gives you a tax break or an exclusion when you sell your house. If you are Married Filing Jointly (MFJ), its $500,000. If you are Single, it’s a $250,000 exclusion on capital gains.

The formula to calculate capital gains on the sale of a house are:

Sales price – Basis = Capital Gains.

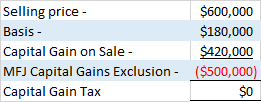

Here is a simple scenario. A couple sells their home for $600,000. They bought the home in 1985 for $180,000 and did no improvements (The improvements would increase the basis). This is what the math would look like.

They would owe NO capital gains tax to the IRS because of the exclusion.

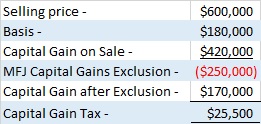

Let’s take the same scenario, everything being equal, except that now the home is sold by a person who is single. The calculation would be as follows:

The selling homeowner would have to pay Capital Gains Tax on the leftover gain after exclusion. The Capital Gains tax rate for most people is 15%. There are three tiers, but 15% is the most common. The Single homeowner will owe approximately $25,500 in tax on the capital gain.

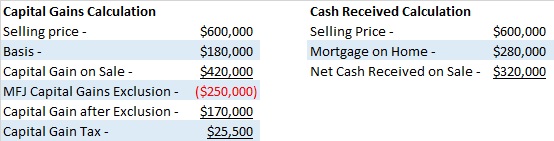

Mortgages. The capital gains calculation has nothing to do with how much you owe on your mortgage, unless you have used the mortgage to improve your home. If the mortgage was used to buy cars, pay off debt, etc. it cannot be added to the basis of the home when calculating capital gains. Here is the same scenario on capital gains, and the actual cash you receive from selling your home. In this scenario the single person, took out a second mortgage to pay off $100,000 in student debt.

The home seller would still pay the $25,500 in Capital Gains Tax from their proceeds of $320,000.

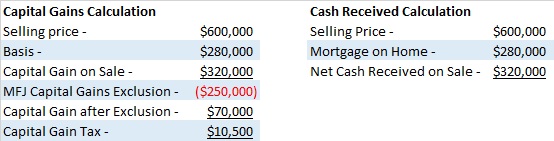

Let’s use the same scenario, but the homeowner took out a $100,000 second mortgage and added two rooms to the house and improved the value. Here would be the calculation.

There are a few sites on the web that can help with Capital Gains on the Sale of a Home calculators. Here is one of them, http://www.homegain.com/sellertools/capital_gains_calculator.

In all of these scenarios, because of the generous $500,000 exclusion for married couples filing jointly, there would be no Capital Gains Tax paid by them.

Selling your home can be confusing. Hopefully these simple calculations will help you do decide the best way to lower your capital gains tax liability, and take the mystery out of selling your home.

Comments